Thirty-Four Dollars: Sri Lanka’s Economic Recovery

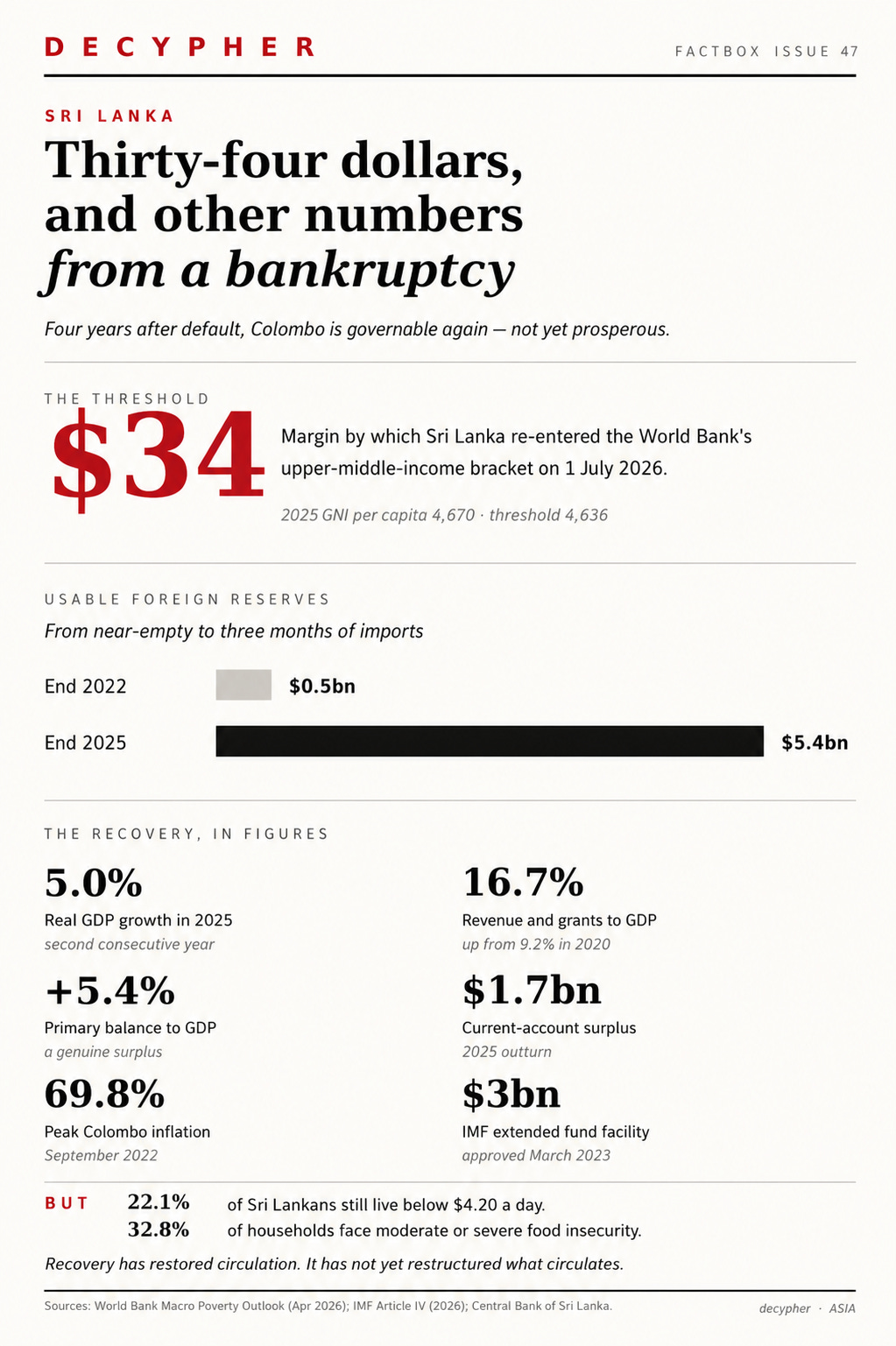

Sri Lanka returned to the ranks of upper-middle-income countries by thirty-four dollars. The figure carries the authority of a verdict and the slight absurdity of an accounting error. Under the World Bank classification that took effect on 1 July 2026, Sri Lanka’s gross national income per capita for 2025 was $4,670. The threshold was $4,636. No economy feels transformed by an additional thirty-four dollars, but statistical categories do. Four years after defaulting on its foreign debt, rationing petrol and watching its president flee the country, Sri Lanka found itself in another column of the global ledger.

It is a return rather than a first ascent. Sri Lanka had entered the same category in 2019 and slipped back the following year. The reclassification captures a genuine recovery in income, growth and institutional control. It contains no memory of the nights spent in fuel queues, of pharmacies without medicine, or of children arranging schoolwork around electricity cuts. National income had travelled far enough to cross a line. The people gathered inside the average had not all travelled the same distance. At the height of the shortages, the Sri Lankan state appeared on a telephone screen. The National Fuel Pass assigned each registered vehicle a QR code and a weekly petrol allocation. It created no fuel. It imposed sequence upon scarcity: this vehicle before that one, this many litres and no more. For a few months, one of the state’s most intimate functions was to decide how far a citizen could travel.

Seventy years earlier, scarcity had been administered through another object small enough to fit in the hand. The rice ration book carried the assurance that the staple around which domestic life revolved would remain within reach. When the government increased the price of rationed rice from 25 to 70 cents a measure in 1953, trains stopped, roads were blocked, and workers stayed away. The Hartal of 12 August turned the price of a meal into a judgment on the meaning of independence. The ration book and the QR code belonged to different political worlds. The first emerged from a state that extended its authority through welfare; the second from one that tried to preserve its authority after bankruptcy. Both reveal the intimacy of Sri Lanka’s economic history. A shortage rarely remained inside the Treasury or the Central Bank. It moved into the rice pot, the schoolroom, the bus journey and, eventually, political allegiance.

Sri Lanka’s postcolonial state had made a social promise larger than its modest income appeared able to support. Free education, public healthcare, food subsidies and social services were not rewards postponed until industrial prosperity arrived. They were intended to create a more equal society before the country became rich. The achievement unsettled the assumption that growth must precede welfare. A child born on a relatively poor island could expect schooling, medical care and a life considerably longer than income alone predicted.

Laksiri Jayasuriya described this settlement as a form of social citizenship. A public hospital did more than deliver a service; it instructed citizens in what government was for. Subsidised rice placed the state at the family meal. Free education opened routes of social mobility, although language policy, regional inequality and the disenfranchisement of plantation Tamils revealed how unevenly citizenship had been distributed. Welfare widened belonging while the same state drew exclusions around it.

Later accounts sometimes treated this arrangement as Sri Lanka’s original economic sin: a poor country promising too much, then borrowing for decades to avoid admitting that it could not afford the promise. Schools and hospitals did not bankrupt the island. The deeper weakness lay in the productive and fiscal structure beneath them. Sri Lanka became more successful at distributing the social gains of development than at transforming the economy required to sustain them. The island remained exposed to the world beyond it. Colonial Ceylon earned foreign exchange through tea, rubber and coconut. Garments, tourism and migrant labour later broadened those earnings without ending their vulnerability. Fuel, medicine, machinery, fertiliser and many inputs needed for domestic production still had to be purchased in foreign currency. The economy could appear settled in rupees while growing anxious in dollars. This gave Sri Lankan politics a distinctive relationship with time. When foreign currency became scarce, governments could impose changes with immediate costs or wait for the next inflow. They became highly practised at waiting. A weak export year might be repaired by a better tourist season. Remittances could compensate for jobs that the domestic economy had not created. A loss-making public enterprise could survive because reform would disturb workers, consumers and political appointments at once. Borrowing allowed each problem to be advanced without requiring the entire structure to be confronted. Financial rot accumulated through these comprehensible postponements. It was not a secret illness discovered in 2022. It was the public habit of refusing to make several weaknesses visible simultaneously.

Saman Kelegama’s account of post-independence development approached the economy from this side of the dilemma. He saw recurring foreign-exchange constraints, limited productive transformation, electoral pressures and conflict. Read beside Jayasuriya, his argument removes the false choice between celebrating welfare and blaming it. Sri Lanka’s social settlement deserved preservation. The economy beneath it remained perilously shallow.

The opening of the economy in 1977 changed how that contradiction was managed. Imports returned to shop windows, garment factories expanded, tourists arrived, and migration connected rural homes to wages earned in the Gulf. J. R. Jayewardene offered consumption as proof that scarcity had ended, while the new executive presidency concentrated the authority through which the open economy would be governed. Markets widened, yet the state did not disappear. Public employment, subsidies, and state enterprises survived alongside contracts, licences, and opportunities distributed through political proximity.

The civil war hardened this political form. It enlarged the military, normalised emergency rule and secrecy, and accustomed the executive to treating scrutiny as an obstacle to national survival. Its costs were never merely fiscal. The north and east endured destruction, displacement and the erosion of livelihoods; elsewhere, the war allowed national indicators to coexist with sharply different regional economies. As analyses of Sri Lanka’s hybrid political regime have shown, the conflict did not mechanically cause the default thirteen years after it ended. It shaped the state that would later meet economic danger: centralised, securitised and impatient with disagreement.

When the war ended in 2009, the Rajapaksa government did not simply claim a peace dividend. It transferred the language of victory into development. Roads, ports, airports and a remade Colombo would bind the island materially after the state had defeated the challenge to its territorial authority. Mahinda Rajapaksa’s political character suited the moment. He spoke with rural familiarity while presiding over concentrated power; the family appeared less as temporary occupants of office than as custodians of the national future.

Concrete made that claim visible. Infrastructure had genuine uses, and Chinese lending alone cannot explain the bankruptcy. The more consequential shift was Sri Lanka’s growing reliance on international sovereign bonds and other commercial debt, which arrived quickly and demanded repayment on shorter, less forgiving terms than concessional loans—borrowing compressed political time. A port could rise before the economy around it existed; the prestige of development arrived immediately, while repayment belonged to a future government. Saman Kelegama examined the politics and contradictions of this period in his study of the Rajapaksa decade.

Gotabaya Rajapaksa inherited the family mythology but not his brother’s political elasticity. Elected in 2019 after the Easter bombings, he offered the severe competence of a former defence official. His preference for command over negotiation shaped the mistakes that followed. According to the IMF’s 2022 assessment of Sri Lanka, government revenue and grants fell from 12.6 per cent of GDP in 2019 to 9.2 per cent in 2020, while the fiscal deficit widened from 8 to 12.8 per cent. Tourism had already weakened; the pandemic then emptied hotels and shut Sri Lanka out of international capital markets. The government attempted to preserve stability by defending the exchange rate, restricting imports and financing spending through the central bank. The fertiliser ban of 2021 revealed the same governing instinct. A difficult agricultural transition was declared as an immediate national transformation, with farmers expected to reorganise cultivation at the speed of an executive announcement. The larger crisis was already taking shape. Sri Lanka was losing the dollars needed to sustain an import-dependent economy, and its rulers were losing credible means of obtaining them.

Debt service continued while reserves disappeared. Import controls concealed a shortage of foreign currency by converting it into shortages of goods. In April 2022, the government suspended external debt payments. By the end of that year, usable reserves had fallen to about $500 million, according to the World Bank’s April 2026 Macro Poverty Outlook. Adjustment had not been avoided; it had been delayed until it could occur only through collapse. By September, Colombo inflation had reached 69.8 per cent and food inflation 94.9 per cent. Inflation at that scale changes the character of time inside a household. A salary ceases to be a monthly quantity and becomes something that loses meaning each day it remains unspent. Savings accumulated over the years can disappear if not used; the future contracts to the next purchase.

Families became the shock absorbers of the economy. Meals were simplified, medicines were rationed, and purchases were postponed. Those with dollars or relatives abroad inhabited depreciation differently from those dependent on fixed rupee wages. Women carried much of the unpaid work created when transport, public services and consumption failed together; the country’s main foreign-exchange earners in garments, plantations and migrant labour already depended heavily on their paid labour. As Kanchana Ruwanpura, Bhumika Muchhala and Smriti Rao have argued, the debt crisis was also gendered. Remittances appeared as resilience in the balance of payments, but they were wages earned through absence, and households reorganised across borders.

The Aragalaya grew out of this exhaustion, though it was never solely a protest against prices. “Gota go home” gave a long crisis a name because political movements require a scapegoat. When protesters entered the presidential residence, the contrast between public scarcity and private abundance briefly occupied the same rooms. The movement removed a president and broke the authority of a family that had made itself difficult to distinguish from the nation. Gotabaya Rajapaksa fled the country in July 2022, but the movement could not restructure a bond.

Ranil Wickremesinghe represented another political temperament. He belonged to the old Colombo establishment, spoke the language of institutions and international finance, and possessed little popular intimacy. Parliament elected him with support from the formation the streets had rejected. His government restricted protest, but it also accepted the facts the previous administration had resisted: the debt could not be paid as contracted, the currency could not be permanently defended, and the state could not recover without collecting more revenue.

The $3 billion IMF programme approved in March 2023 formalised that recognition. Debt was restructured; taxation increased; fuel and electricity prices moved closer to cost; monetary financing was curtailed; the exchange rate became more flexible; and the central bank gained greater autonomy. These were not rituals performed solely for creditors. A state without reserves cannot import medicine through goodwill, and inflation punishes households whose incomes cannot be renegotiated. Necessity did not determine distribution. Indirect taxes reached into consumption. Electricity tariffs moved losses from public accounts into household and business bills. Currency depreciation compressed imports because people could afford fewer of them. The government balance sheet and the family budget were repaired through the same process. Costs earlier borrowed, subsidised, or concealed reappeared in higher tax payments, higher prices, and diminished consumption.

Aswesuma gave this relationship an administrative form. The new welfare programme sorted applicants into transitional, vulnerable, poor and severely poor groups. Targeting promised to reduce the patronage and leakage associated with Samurdhi. It also required deprivation to become legible before it produced an entitlement. The World Bank’s Public Finance Review later found that district allocations still relied on 2019 poverty patterns, although the crisis had altered where insecurity lived. A family could become poor faster than the database could learn its new condition. The recovery was nevertheless real. By the end of 2025, usable reserves had risen from roughly $500 million to $5.4 billion, enough for about three months of imports. The economy had grown by 5 per cent for a second year; the current account recorded a $1.7 billion surplus. Government revenue and grants reached 16.7 per cent of GDP, and the primary balance moved to a surplus of 5.4 per cent. These figures, recorded in the World Bank’s April 2026 economic assessment, described a state that had regained substantial control over itself. Fuel queues disappeared, medicine returned, and firms could plan purchases without wondering whether the rupee would lose another portion of its value before a shipment arrived. The figures also contain quieter stories. The unusually large primary surplus reflected strong tax collection, especially after vehicle imports resumed, and the under-execution of capital spending. Reserve accumulation rested on tourism and remittances, including the labour of citizens who had left. As the IMF’s 2026 review makes clear, recovery restored circulation: dollars entered, imports arrived, taxes were collected, and obligations were renegotiated. It did not yet answer whether the economy producing those flows had changed.

Anura Kumara Dissanayake’s election in 2024 promised a political break from dynasties and the established parties. His National People’s Power coalition won 159 of 225 parliamentary seats. Yet his government retained the central framework of the IMF programme. Bankruptcy had narrowed the range of credible rupture. A new administration could alter priorities, expand protection and confront corruption; it could not behave as though default had never happened. Wickremesinghe imposed discipline without a popular mandate. Dissanayake inherited a mandate for change within limits drawn by creditors and by the memory of empty filling stations.

This constrained recovery met its first major test not in a negotiation room or a bond market, but in rain. Cyclone Ditwah made landfall on 28 November 2025, bringing prolonged rainfall, floods and nearly two thousand landslides. By 19 January, 646 people had died, and 173 remained missing. Close to two million people were affected across the island, while homes, farms, roads, railways and water systems were damaged. The storm arrived just as the figures of recovery appeared most persuasive. The World Bank’s rapid assessment placed direct physical damage at $4.1 billion, approximately 4 per cent of GDP. That figure could record a destroyed bridge or flooded house, but not the wages lost while roads remained impassable, the debt assumed to repair a roof, or the cultivation season that could not be recovered. Ditwah did not cause Sri Lanka’s bankruptcy. It changed the meaning of recovery. Reserves and tax revenues had improved just as reconstruction created new fiscal and foreign-exchange demands.

Sri Lanka therefore returned to the IMF while the existing Extended Fund Facility remained in place. In December 2025, the Fund approved approximately $206 million through its Rapid Financing Instrument. The contradiction was immediate: a state that had created fiscal room through higher taxation, restrained spending and the under-execution of capital budgets now required precisely the public investment that consolidation had limited. The burden also fell upon households that had not recovered from the original crisis. In 2025, 22.1 per cent of Sri Lankans remained below the World Bank’s $4.20-a-day poverty line, while 32.8 per cent of households experienced moderate or severe food insecurity. The Middle East conflict poses a secondary danger by raising commodity prices, disrupting essential supplies, and weakening tourism and migrant earnings. Ditwah was the immediate test. Sri Lanka became governable again, but the cyclone asks whether a state trained by bankruptcy to tax, target and restrain can also rebuild, protect and invest without requiring vulnerable households to absorb another national emergency.

Sri Lanka did not travel from bankruptcy to prosperity in four years. It became governable again. That achievement matters to anyone who remembers the queues, because predictable prices, available fuel, and a currency able to purchase medicine are forms of security. Yet governability is not a renewed social compact. The state has recovered its ability to measure, tax, target and restrain. It has not shown that these capacities will create an economy less dependent on borrowed time and the departure of its workers.

Essay: Preksha Jalan- Associate Fellow, Digital History Lab at The Advanced Study Institute of Asia (ASIA), affiliated with SGT University, Gurugram.

Produced by Decypher Team in New Delhi, India