The Geopolitics of Offshore Renminbi

By Amogh Dev Rai | Research Director and researcher on China, and Chinese Geopolitics.

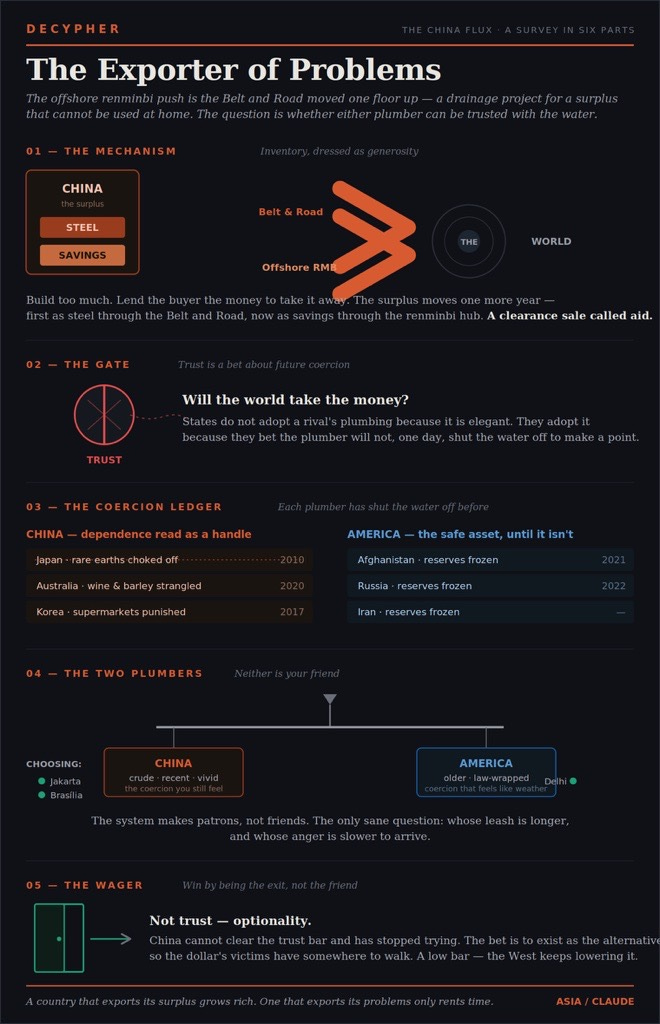

Every empire that runs out of room at home goes looking for it abroad, and always under a kind name. The British called it trade. The Americans called it the order. The Chinese call it the Belt and Road, and now the offshore renminbi hub, and the second is the first in a banker’s coat.

Look at how the Belt and Road actually ran, not how the declarations sold it. China had built too much. Too much steel, too much cement, too many firms and provincial officials whose careers were poured in concrete, and not enough demand at home to use any of it. A factory tooled for forty thousand kilometres of rail cannot live in a country needing four thousand more. So you find other countries to take the rail. You lend them the money to buy it. You send your own firms to lay it. The loan comes home as profit; the rail stays in Sri Lanka or Kenya; the overcapacity is exported for one more year. It looked like generosity. It was inventory management.

The offshore renminbi push is that same move, one floor up, where the suits are better and the problem is harder to photograph. The surplus this time is not steel. It is savings. China saves enormously and trusts itself too little to spend. For thirty years the money went into apartments. Now the apartments don’t sell, the developers are going broke if not already, the local governments that lived off selling land have no land income left, and the great river of Chinese savings has nowhere good to go. Not much to buy for they are worried about their economy. Fixed-asset investment turned negative this spring. Property is still falling.

So Beijing does upstairs what it did down: builds a channel and sends the surplus out. Let the renminbi flow offshore, lent and settled and hedged in Shanghai and Hong Kong. Find the world somewhere to park the money the Chinese themselves can’t put to work at home.

That is what the Lujiazui Forum tried to achieve.

Now the question the financial press never asks, because it is not a financial question. Will the world take the money? Allow me a (bad) plumbing analogy.

States do not adopt another state’s plumbing because it is elegant. They adopt it because they bet the plumber will not, one day, shut the water off to make a point. Trust is not a feeling. It is a wager about future coercion. And the Belt and Road decade is now a ledger of that wager. China has been slightly deficient with respect to that.

Sri Lanka handed over a port on a ninety-nine-year lease, and the word that travelled was trap — and in this business the belief in a trap does a trap’s work, whether or not the thing was ever sprung. Zambia defaulted. Pakistan, the flagship, the all-weather friend, has spent the years since renegotiating and quietly begging while the power plants China built sit dark because Pakistan cannot pay for fuel. The borrowing countries learned, in the only school that teaches this the one you enter after you have already signed that the capital came with Chinese contractors, Chinese specifications, and a lien if you missed a payment. The deals were not uniquely cruel. They were deals, inside a thing the declarations had called friendship, and finding out it was a deal is what puts the mis in the trust. You do not forgive the bank that forecloses the way you forgive the friend who lent. China wanted to be both, and now it has a choice to make.

So when that same state says hold your reserves in our currency, route your savings through our hub, the courted countries do the arithmetic they didn’t know to do the first time. They ask what happens the day Beijing is displeased. They have the answer. They watched China choke off rare earths to Japan over a fishing boat. It was never openly declared, they choked them in bureaucratic export controls. They watched it strangle Australian wine and barley over a request to look into a health concerns. They watched it punish Korean supermarkets over a missile battery. The renminbi system asks for trust from a state that has shown, recently and often, that it reads economic dependence as a handle to pull.

Now turn the knife on your own side, because the West is reading this and feeling safe. Is the dollar a good partner? The United States froze Afghanistan’s reserves, then Russia’s, then Iran’s. Each freeze was lawful in its own logic. Each also taught every central banker in office that the safe asset is safe until Washington decides you are. The dollar was the neutral water everyone drank. The Americans have been poisoning that well themselves, freeze by freeze, for small wins — to punish a war, to squeeze a regime — without noticing that the thing they spend is the only thing that made the dollar worth more than gold: the belief that it stood outside politics. Everyone now knows it does not. That knowledge is the largest gift the West has handed the Chinese project, worth more than anything Pan Gongsheng could announce.

So here is the real shape, uglier than the triumph the bulls sell or the collapse the bears promise. The world is choosing a plumber between two states that have each, within memory, shut the water off to make a point. China is the newer offender, the recent one, the one whose coercion is still vivid. America is the older one, whose coercion comes wrapped in law and habit until it feels less like coercion than like weather. Neither is your friend. The system makes patrons, not friends, and the only sane question in Jakarta or Brasília or Cairo is whose leash is longer and whose anger is slower to arrive.

China is betting it can win that not by being trustworthy, it has shown it cannot be fully trustworthy but by being the exit, by simply existing, so the dollar’s victims have somewhere to walk even if the new house has a landlord too. A low bar. Possibly a winning one, because the West keeps lowering it.

The Signals

The Action Plan for the Development of Offshore Finance at the Shanghai International Financial Centre, jointly issued by six bodies (PBOC, NDRC, NFRA, CSRC, SAFE, Shanghai Municipal Government). Three-stage timeline: an initial system by end-2027, a “relatively mature” framework by end-2030, and Shanghai as a strategic onshore–offshore hub by end-2035. The design principles are the analytically important part — 物理集聚 (physical agglomeration), 主体限定 (entity restriction), 账户隔离 (account isolation), governed by 两头在外 (”both ends outside”). This is a controlled membrane, not an open door.

The doctrinal phrase to watch. 制度型开放 — “institutional-type opening” — paired consistently with 统筹金融发展和安全 (”coordinating financial development and security”). SAFE chief Zhu Hexin described the mechanism shift openly: from prior approval to in-process monitoring and after-the-fact verification (从事前审核向事中监测事后核查). The control is relocated, not removed.

The Hong Kong dimension. A signed Shanghai–Hong Kong Coordinated Development Action Plan (38 measures) formalises the division of labour: Shanghai as the onshore allocation centre, Hong Kong as the offshore RMB hub. Stated goal: raise China’s 话语权 — discourse power — in the global financial system.

Market reaction. SSE Composite closed at 4,110 on 17 June (+0.44%). Zhipu AI jumped 33% on an open-source model release. The e-CNY internationalisation push extended cross-border digital-yuan payments toward Singapore, the UAE, and Brazil.

The counter-signal (what the forum was staged to obscure). The USCC bulletin (9 June) reported fixed-asset investment turned negative in April, property rates declining, and local governments diverting infrastructure bonds to service hidden debt. The forum is the moat being build.

Produced by Decypher Team in New Delhi, India