How Trump’s Foreign Policy Is Reshaping China’s Global Standing

This week, we examine how China’s influence is reshaping global markets, altering geopolitical alignments, and quietly laying the groundwork for ambitious resource plans that extend far beyond Earth.

Is Trump Making China Great?

The European Council on Foreign Relations has put out a fascinating survey of 25,949 respondents across 21 countries. The survey points to a change that is happening in global politics in front of our eyes. Very rarely in history do we see a rebalancing not of power structures but a permissive realignment of what countries now perceive that they are allowed to do. We also analyse James Schneider’s essay in The Newstatesman where he argues that Britain has to extend the logic of special relationship beyond the United States. Let us break it down.

I. The Permission Structure

The ECFR headline is blunt: “Trump is making China great again.” But it’s the structure, not the slogan, that’s more significant.

What the data actually reveal is this: in Brazil, South Africa, Turkey, Russia, and even India, majorities believe that their countries can simultaneously maintain good relations with both Washington and Beijing. Not as a hedge. Not as a way of nervously balancing between the two. But as the new normal. Two years ago, this was a minority position in all of these countries. Now, it’s just common sense.

The permission was not granted by Beijing’s charm offensive. It was granted by the abdication of Washington. By treating the “liberal international order” as an optional bylaw that applies to the United States but not to itself, while insisting that everyone else make a choice between Washington and Beijing, Trump has effectively freed the middle powers from the need to pretend that there is still a coherent “West” to line up behind.

The logic of Schneider’s argument here is the same as the one from the British perspective: “The pretence of a rule-bound order has given way to something cruder.” Brexit has destroyed the European pillar of British foreign policy; Trump is now undermining the American one. What remains is a dependency without returns—strategic subordination to Washington that no longer even provides predictable behavior on the part of the alliance. But here’s the kicker. The ECFR data also show that 37% of Russians now consider the US an adversary. That’s down from 64% two years ago. Meanwhile, Europeans have become the enemy in Russian eyes. As Trump woos Putin, Russians are readjusting their threat calculations accordingly. This is not opinion. It’s strategy made visible in public opinion.

Putin’s move, as one Russian strategist told the ECFR, according to the brief: “Keep the Europeans out, the Americans in, and the Ukrainians down.” In other words: let the Americans do the heavy lifting of dealing with European pushback while Moscow locks in its gains.

The geometry of all this is far from obvious. Trump’s transactional politics are not building a US-Russia bloc (Americans still overwhelmingly regard Russia as an enemy). What they are doing is decoupling transatlantic threat perceptions—building a license for selective engagement while the old alliance framework freezes in rhetoric but not in fact.

II. The India Problem

The most telling piece of data in the ECFR survey: Indian optimism about Trump plummeted from 84% (late 2024) to 53% (late 2025). That’s a 31-point fall in one year.

But the most telling piece of data of all: nearly half of Indians now regard China as either an ally or a necessary partner. This, with territorial disputes still unresolved. This, with the Quad still in place. This, with the entire Indo-Pacific strategy framework based on Indian cooperation to balance against Beijing.

What’s changed? The survey doesn’t say. But the timing suggests Trump’s tariff war (steel, aluminum, and then the general one), the abandonment of any predictable trade framework, and a growing recognition in New Delhi that Washington’s “partnership” is increasingly a protection racket.

For ASIA’s purposes, this is the most important piece of data in the survey. If the Indian elite and public opinion are both trending towards an accommodation with China—not because they like China but because they’re pragmatists—then the entire debate about “Quad solidarity” has to be rewritten.

We’ve been assuming that Indian strategic autonomy implies equal distance between Washington and Beijing. But what the ECFR data indicate is something different: Indians are increasingly seeing the US as more unpredictable and transactional than China. That’s a preference ordering, not just non-alignment.

III. Europe’s Perception Gap

This is where the ECFR data gets really strange: citizens in South Africa, Brazil, China, and Ukraine all see the EU as a major power that can act independently. Europeans do not.

In particular: most Europeans think the EU “cannot deal on equal terms with the US or China”—and this has gotten worse over the last year. At the same time, 61% of Chinese consider the US a threat, but only 19% consider the EU a threat. Chinese respondents increasingly see EU policies towards China as different from US policies—a staggering change from just two years ago, when most Chinese saw them as the same thing.

This produces a strange kind of symmetry. Beijing is already treating Brussels as a separate pole. Brussels has not yet absorbed this reality. Schneider’s article does not address this, but Schneider’s critique of British elite consciousness follows the same pattern: “Britain’s ruling elite retains imperial instincts because it lacks a material agenda for transformation.” Again, the same could be said of Europe as a whole. The architecture for multipolarity is already in place (separate trade policies, regulatory independence, different diplomatic stances). The imagination for it is not.

What the ECFR data shows is that this is, first and foremost, a European problem. The rest of the world has already passed them by. They’re not waiting for Europe to become a pole. They’re treating it as one and acting accordingly.

IV. What Schneider Gets Right (and Wrong)

The underlying thesis of Schneider’s piece is that Britain’s stagnation is a tale of dependency, and that a “new relationship with China” is part of a strategy to end managed decline. The argument is stronger than it initially seems. His take on Cameron’s China policy as “inviting Chinese capital into British assets in order to juice the City—engagement without production, partnership without construction” is spot on. What’s important isn’t whether Britain speaks to Beijing. It’s what they get out of it.

Where Schneider is absolutely right: “You cannot build a green economy while pretending the world’s manufacturing centre does not exist.” China dominates the supply chains that are materially necessary for decarbonization—solar, batteries, rare earths, and grid infrastructure. This isn’t about ideology. It’s about material reality.

The steel analogy is helpful. Britain came perilously close to losing all its primary steel production in 2025 when the Scunthorpe blast furnaces were almost shut down by their private Chinese owner. Schneider’s point that steel needs to be treated as infrastructure, not as property that can be held by people with short time horizons, isn’t protectionist. It’s a recognition that certain kinds of industrial capacity are antecedent to everything else.

But Schneider gets slippery here, from “Britain needs productive engagement with China” to “China’s external behavior is more predictable and peaceful than Washington’s” to “a country that arms Israel cannot lecture China on Xinjiang.” The rhetorical move from one to the next has a certain persuasive power that the evidence doesn’t quite support.

It is, of course, the case that the US has over 800+ military bases around the world and has intervened militarily in at least seven countries in the last year. It is also the case that the external behavior of the Chinese state is one of long-term stability rather than kinetic action. However, “predictable” is not the same thing as “benign,” and while it is true that Schneider could highlight the hypocrisy of the West regarding human rights, this does not make the Chinese government’s repression of its citizens disappear—it simply shifts the moral pain.

What Schneider is actually advocating, although he does not quite put it this way, is that the UK should follow the same stance that majorities in Brazil, Turkey, South Africa, and Russia have already taken, according to the ECFR data, and that is to view human rights as a universal concern rather than a geopolitical tool, and to seek material partnerships based on mutual advantage rather than ideological compatibility.

This is principle masquerading as pragmatism. Which is just fine, actually. Pragmatism gets a bad rap. But let’s not pretend it’s something else.

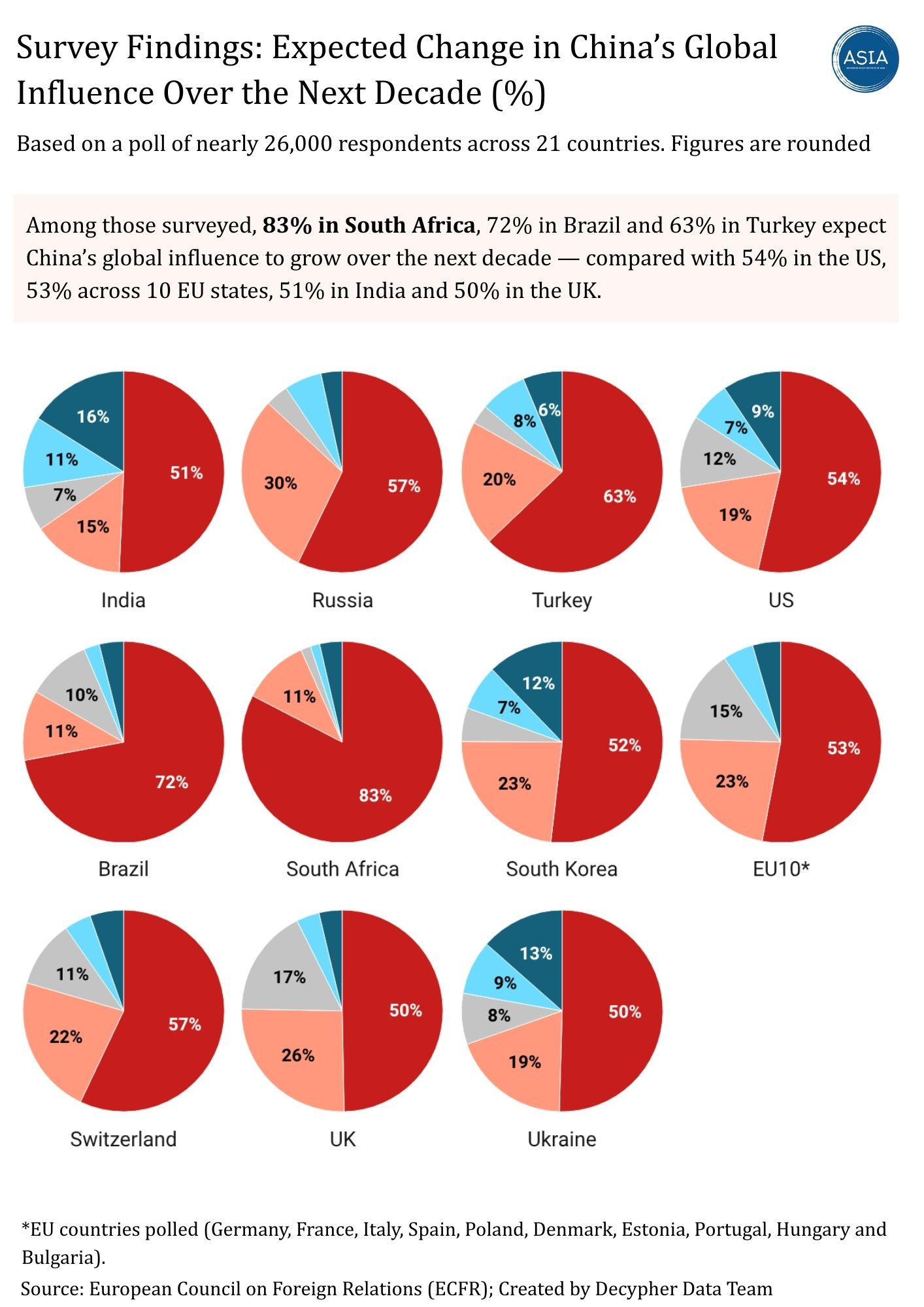

According to an analysis by the European Council on Foreign Relations (ECFR), many people around the world expect China’s already considerable global influence to grow over the next decade, and more now view Beijing as an ally or a necessary partner.

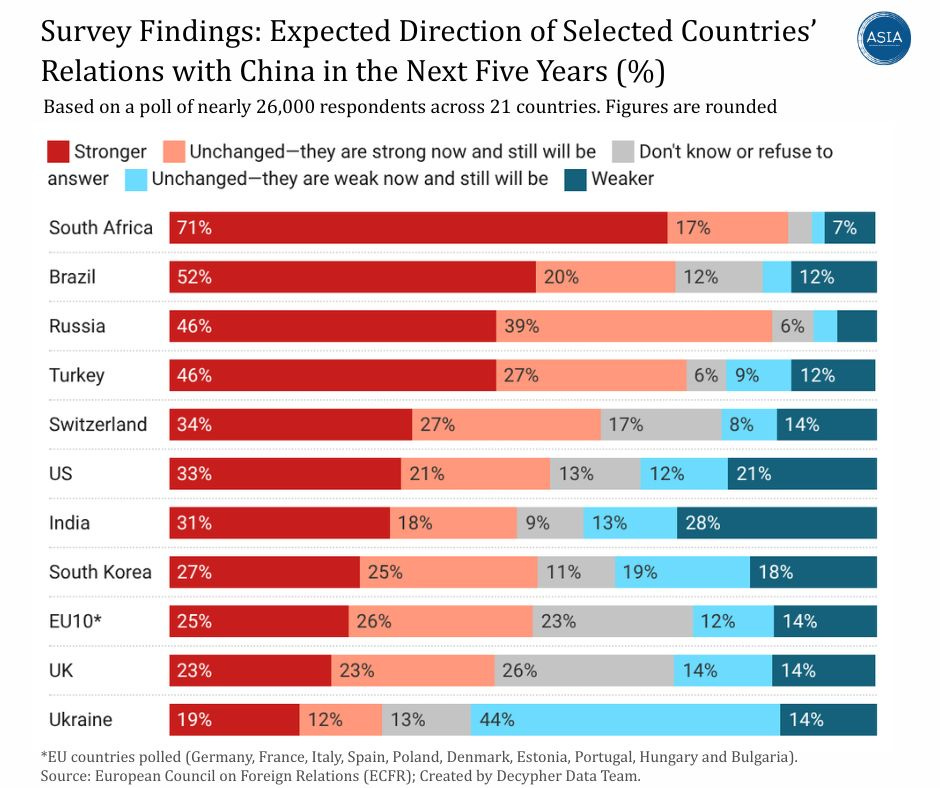

In several countries, many respondents expect their country’s relationship with China to strengthen over the next five years. Clear majorities in South Africa (71%) and Brazil (52%) say this, while sizable shares in Russia and Turkey also anticipate closer ties.

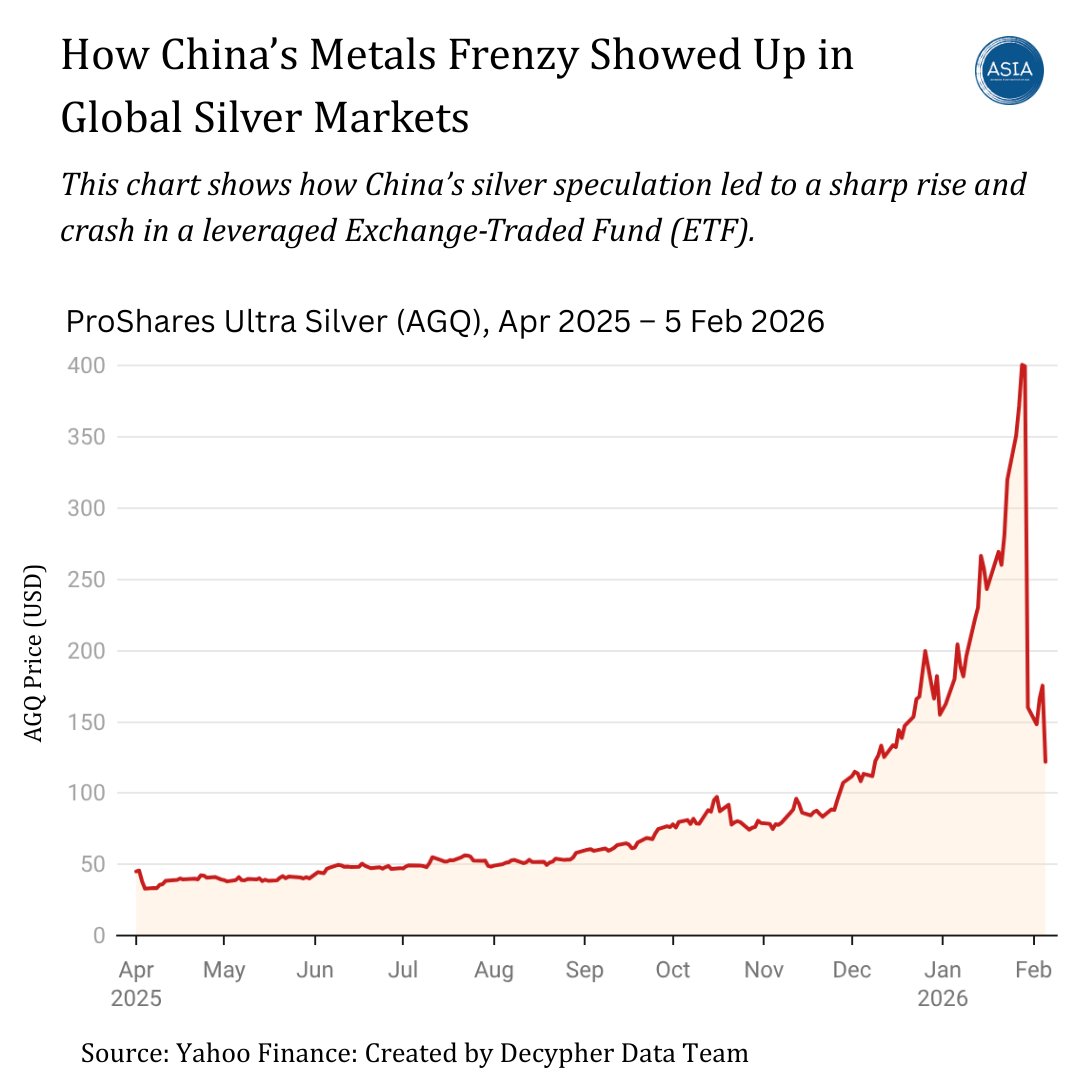

Commodity Boom in China

Retail investors in China rushed into metals like gold, silver, copper and tin, creating sharp swings in global commodity prices. With few attractive options at home and social media amplifying the excitement, many treated commodities as a quick trading opportunity rather than a long-term investment.

Global price movement was swiftly impacted by this spike in trading activity in Shanghai futures markets. The fast increase and then decline in ProShares Ultra Silver (AGQ), a 2× leveraged silver ETF traded in the US, as international investors responded to swift price swings, was one obvious manifestation of this volatility.

A $1 billion withdrawal from gold ETFs in a single day, record futures trades in Shanghai, and large losses for novice traders when prices reversed were all outcomes of the frenzy. This incident was motivated by financial speculation rather than construction demand, despite being reminiscent of China’s steel trade mania in 2016. It shows how Chinese retail flows can now quickly impact global commodities markets.

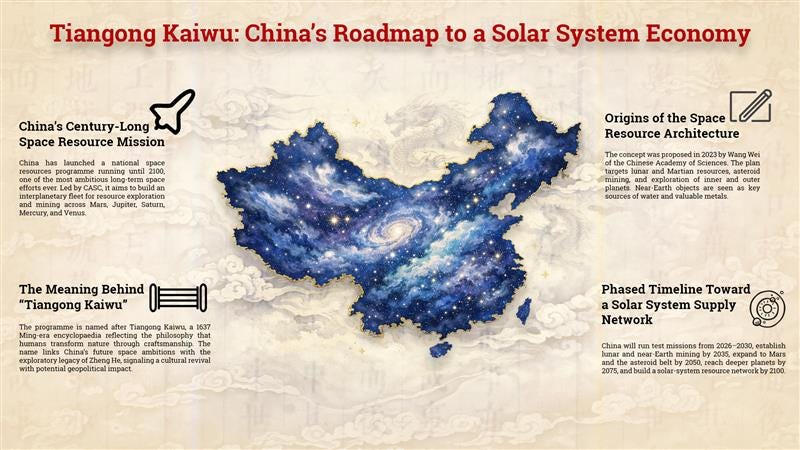

China’s Race to Space

China has launched a national space resources development programme that will run until 2100, making it one of the most ambitious long-term space projects ever announced. Led by the China Aerospace Science and Technology Corporation (CASC), the plan aims to build a large interplanetary fleet to support resource exploration and mining across the solar system, including Mars, Jupiter, Saturn, Mercury, and Venus.

The programme is named after Tiangong Kaiwu (“The Exploitation of the Works of Nature”), a major encyclopaedic work published in 1637 during the Ming dynasty. The name reflects the Ming scientific philosophy that “materials are born of nature; humans transform them through craftsmanship.” It also symbolically connects China’s future space ambitions to the historic voyages of Admiral Zheng He, extending the idea of exploration from the seas to the entire solar system. This growing interest in reviving Ming dynasty-inspired thinking reflects a broader cultural shift that may have far-reaching implications for the future geopolitical landscape.

The concept was first proposed in 2023 by Wang Wei of the Chinese Academy of Sciences in a research paper on space resource exploitation architecture. The long-term goal is to develop systems for lunar and Martian resources, mine near-Earth and main-belt asteroids, and explore gas giants and inner planets. Wang noted that near-Earth objects contain water and valuable metals such as nickel, platinum, and gold.

From 2026–2030, China will conduct demonstration missions to test feasibility. By 2035 it aims to establish lunar and near-Earth mining systems, expanding to Mars and main-belt asteroids by 2050. By 2075, it expects capabilities for deeper exploration of Jupiter, Saturn, Mercury, and Venus, and by 2100 it plans a full solar-system resource supply network.

— — —

Essays: Amogh Dev Rai and Neeti Goutam

Data and Visualisation: Bhupesh and Raghav

Produced by Decypher Team in New Delhi, India

— — —